The Basics of Budgeting & Expense Tracking

.webp)

Budgeting and expense tracking are often used interchangeably, but in reality, they are two distinct concepts with complementary roles. Many people assume that once they create a budget, the work is done. In practice, however, without tracking expenses, a budget remains nothing more than a plan on paper.

Michael had just arrived in Dubai.

He came from a place where the value of money was fragile. For years, he had lived with constant financial uncertainty, carefully watching every expense, postponing savings, and never feeling fully secure about the future. Dubai represented a fresh start for him, a city where money held real value, opportunities were tangible, and income could finally be earned in strong global currencies.

During the first few months, everything seemed to be going in the right direction.

Michael was earning well. His income was stable, paid on time, and denominated in dollars. For the first time in his adult life, he felt a sense of financial relief. The pressure he had carried for years slowly faded, replaced by confidence and optimism.

But that feeling did not last long.

After several months, Michael began to notice something unsettling. Despite earning a solid income, the numbers at the end of each month were not what he expected. His money was not disappearing suddenly. He was not overspending recklessly. He was not buried under debt. His wallet was not “leaking,” and his income was not melting away.

Yet, month after month, he was not moving forward.

This contradiction bothered him deeply.

How could someone earning a dollar-based income in a city like Dubai feel financially stuck? Michael was not failing, but he was not progressing either. His money seemed to pass through his life without creating momentum.

That was the moment he realized an uncomfortable truth:

the problem was not income.

The problem was structure.

After several conversations and reflections, Michael decided to seek professional guidance. This decision led him to the financial consulting team at Daraltharwa. Contrary to his expectations, the initial discussions were not about complex investments, market timing, or high-risk opportunities. Instead, the focus was placed on something far more fundamental — cash flow behavior.

The consultants asked simple but revealing questions:

- Do you know exactly where your money goes every month?

- Is your spending intentional or habitual?

- Which expenses are essential, and which are quietly draining your finances?

If nothing changes, where will your financial life be in five years?

He had never truly learned how to budget

Michael struggled to answer clearly.

He had never truly learned how to budget. He assumed that once income reached a certain level, financial progress would happen automatically. What he did not realize was that without a system, income alone does not create wealth.

During one of the sessions, Dr. MHS made a statement that changed Michael’s perspective entirely:

“If you don’t understand the rules of budgeting, money simply flows through your life. But once you master those rules, money starts working for you.”

Michael understood that his issue was not a lack of money, but a lack of direction.

Without budgeting, there was no framework for decision-making. Without expense tracking, there was no visibility into recurring financial leaks. And without these two foundations, even strong income and good intentions could not translate into sustainable growth.

He began to see budgeting not as restriction, but as alignment.Budgeting was about deciding which part of his income supported his current lifestyle and which part was designed to build his future. It was about balancing quality of life with long-term financial security. Most importantly, it was about stopping the silent erosion of wealth the kind that happens slowly and often goes unnoticed until it is too late.

As Michael started tracking his expenses consistently, patterns emerged.

Many of his financial decisions were not conscious choices, but habits formed over time. Once those habits were identified and adjusted, something remarkable happened: his money stopped stagnating. It did not grow overnight, and it did not require risky behavior. Instead, it began to grow steadily and predictably.

Michael had entered what financial consultants often refer to as the wealth creation cycle a cycle that starts with budgeting, continues with expense tracking, and eventually enables smarter financial planning and investment decisions. This cycle is not driven by hype or speculation. It is driven by discipline, clarity, and informed choices.

Michael’s story is far from unique.

Many people arrive in Dubai with strong earning potential and real opportunities. Yet without understanding the fundamentals of money management, they never fully enter the path of sustainable wealth. Income alone does not guarantee progress. Structure does.

This article is written for that exact turning point the moment when you realize that earning more is no longer the solution. What matters is learning how to manage, direct, and grow what you already earn.

In the sections that follow, we will walk through the same principles Michael learned: how budgeting truly works, why expense tracking is essential, and how mastering these fundamentals can transform your financial life from stagnant to steadily growing.

If you follow this journey, you may discover that your money does not need to disappear, shrink, or stand still . It can begin working for you.

If Michael’s situation feels familiar, learning the fundamentals of budgeting is the first step toward financial clarity.

Why Does Budgeting Feel So Difficult at First?

For many people, budgeting is mistakenly associated with restriction, rigidity, or a lower quality of life. When they try budgeting for the first time, it often feels like entering a complicated and pointless process — a path filled with numbers, control, and constantly saying “no” to personal desires. Some even abandon it after a few weeks, concluding that “this approach doesn’t work for me.”

The reality, however, is that budgeting often feels difficult at the beginning — not because it is wrong, but because it challenges long-established financial habits. Much like learning any new skill, what initially appears limiting and exhausting is often the very formula that can bring structure and order to your financial life.

Dr. MHS compares a life without financial planning and budgeting to an untamed horse. A horse that is strong, energetic, and fast — but without direction. Such a horse is neither bad nor weak; in fact, it possesses great power. But without reins, it may take you anywhere, throw you off balance, or waste its energy entirely.

In this analogy, your income is the horse. And budgeting is the rein that gives it direction.

Without reins, the horse runs wherever it wants. Without a budget, money is spent wherever circumstances allow.

Not out of bad intention.

Not out of irresponsibility.

But simply because there is no control.

Budgeting is not meant to stop the horse or reduce its power. Its purpose is to direct that power along the right path. When the reins are in your hands, the horse can move faster, more safely, and with purpose. In the same way, when you have a budget, your money can be guided toward growth instead of gradual erosion.

Many people who move to Dubai find themselves in exactly this situation.

They have strong income, real opportunities, and the potential for progress.

Yet without financial direction, they eventually feel that control is slipping away. They are not failing. They are not going bankrupt. They are simply not moving forward.

Budgeting allows you to clearly see:

- how much of your financial energy is supporting today’s lifestyle

- which portion is meant to build the future

- and where energy is quietly being wasted

At this point, budgeting transforms from a “restrictive tool” into a tool of freedom. Freedom does not mean uncontrolled spending; it means conscious choice.

Just as a trained horse becomes more powerful and reliable, money that is guided by budgeting stops creating stress and begins building stability and security. This is the exact shift many people like Michael . experience once they learn the fundamentals of budgeting.

What Is the Difference Between Budgeting and Expense Tracking?

(Planning vs Monitoring)

Budgeting and expense tracking are often used interchangeably, but in reality, they are two distinct concepts with complementary roles. Many people assume that once they create a budget, the work is done. In practice, however, without tracking expenses, a budget remains nothing more than a plan on paper.

Budgeting is planning before spending.

When you budget, you decide how your money should be used. You determine how much is allocated to essential expenses, how much is set aside for savings, and how much is directed toward future growth.

In contrast, expense tracking is monitoring after spending.

This process shows how your money was actually spent. It reveals whether your real financial behavior aligns with the plan you created.

To make this distinction clearer, budgeting can be compared to a roadmap, while expense tracking functions like a GPS. The roadmap tells you where you want to go, but the GPS continuously shows whether you are staying on course or drifting off track.

In financial consulting experience in Dubai, one of the most common mistakes is that people either create a budget and then ignore it, or they track expenses without having a clear financial objective. Both approaches are incomplete.

Michael initially had only a general sense of his spending. He roughly knew how much he was spending each month, but he did not clearly understand which expenses were essential and which were driven by habit. Once he began tracking his actual expenses, the gap between “what he thought he was spending” and “what he was truly spending” became clear.

This gap is where many financial problems begin. Small expenses, forgotten subscriptions, impulse decisions, and Dubai’s fast-paced lifestyle can quietly place pressure on cash flow without being immediately noticeable.

From a professional perspective, budgeting without expense tracking is like making decisions without data. Expense tracking without budgeting, on the other hand, is like collecting data without purpose. It is the combination of both that enables meaningful analysis, behavioral correction, and ultimately, sustainable financial growth.

For individuals and businesses in Dubai, this combination is even more critical. Variable income, foreign-currency expenses, and changing lifestyles make financial control nearly impossible without real data. Budgeting defines the path; expense tracking ensures you stay on it.

In the next section, we move into the practical stage and explore how to create a simple yet effective monthly budget one that works in real life and does not remain trapped on paper.

This table represents budgeting. It reflects decisions made before money is spent.

The total amount is the same. But the financial story is very different.

What This Comparison Reveals

- The money did not disappear

- Michael was not reckless

- Small, unnoticed expenses quietly reduced savings

If he had only created a budget, this gap would remain hidden.

If he had only tracked expenses, he would not know what needed to change.

📌 The real value lies in comparing both tables.

Without it, money has no direction, Without it, mistakes remain invisible

How to Create a Simple but Effective Monthly Budget

(Without Over complicating Your Life)

One of the biggest mistakes people make when budgeting is trying to build a perfect system from day one. The result is usually predictable: strong motivation at the beginning, followed by frustration, and eventually abandoning the process altogether.

From a financial consulting perspective, a budget that does not start simple will not last. The purpose of budgeting is not to control your life it is to create clarity and direction.

Step 1: Define Your Real Income Baseline

Before anything else, you need to know how much money actually enters your life each month. Not your best month. Not your ideal scenario. The real, repeatable number.

For many people in Dubai, income may be:

- variable

- earned in foreign currencies

- a combination of salary, business income, or project-based work

At this stage, be conservative. Build your budget around the minimum income you can reliably depend on, not the highest possible outcome.

Step 2: Separate Fixed Expenses First

Fixed expenses are costs that repeat every month and leave little room for adjustment, such as:

- rent

- utilities

- insurance

- loan or installment payments

These expenses should be deducted from your income first. Professional budgeting always begins with reality, not optimism.

Step 3: Define Variable Expenses Intentionally

This is where budgeting truly begins to work.

Expenses such as:

- food

- transportation

- entertainment

- daily purchases

These costs are manageable — but only if they are decided in advance. Without prior decisions, variable expenses tend to take control of your financial life.

Step 4: Treat Savings as a Mandatory Expense

One of the most important mindset shifts in budgeting is removing savings from the bottom of the list.

Savings should be treated as a monthly expense, not something you do only if money is left over. Even a small, consistent amount matters more than irregular large contributions.

Step 5: Keep Your Budget Livable

A budget that suffocates your lifestyle will not survive.

If all enjoyment is removed, the system will fail.

A good budget is:

- realistic

- flexible

- aligned with your lifestyle

The goal is gradual progress, not perfection.

Why This Approach Works

Michael started exactly this way.

Not with complex tools or advanced formulas but with a simple framework he could repeat every month.

When a budget is simple:

- it gets implemented

- it can be tracked

- and it can be adjusted

In the next section, we explore the best methods and tools for tracking expenses, from manual approaches to digital solutions that are particularly useful in Dubai.

A Simple Monthly Budget Example (Dubai-Based)

Let’s assume Michael is living in Dubai and wants a clear, realistic monthly budget not a perfect one.

His goal is not aggressive saving or extreme discipline.

His goal is control, visibility, and consistency.

Michael’s Monthly Income (Baseline)

Michael earns a stable monthly income of:

Income: 12,000 AED

(This is his conservative, reliable number not bonuses or exceptional months.)

Step 1: Fixed Monthly Expenses

These are expenses that are difficult to change in the short term.

Fixed Expense

Monthly Amount (AED)

Rent

4,500

Utilities & Internet

600

Insurance

400

Phone

200

Subscriptions

150

Total Fixed Expenses

5,850

After fixed expenses, Michael knows exactly how much flexibility he has.

Remaining balance: 6,150 AED

Step 2: Variable Living Expenses (Planned)

Now Michael decides in advance how much he wants to spend instead of reacting day by day.

Variable Expense

Monthly Budget (AED)

Food & Groceries

1,800

Transportation

900

Dining & Social Life

900

Personal & Lifestyle

600

Total Variable Expenses

4,200

Step 3: Savings and Future Goals

Instead of waiting to “see what’s left,” Michael treats savings as mandatory.

Category

Monthly Amount (AED)

Savings / Investments

1,500

Emergency Buffer

450

Total Saved

1,950

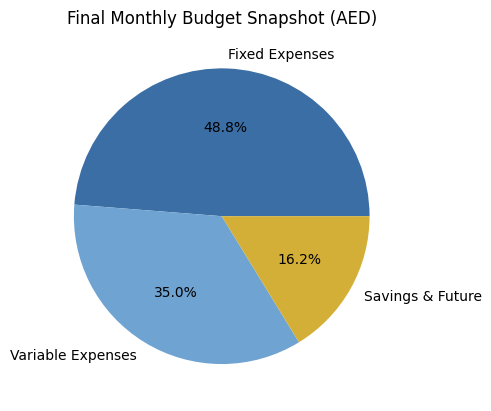

Final Monthly Budget Snapshot

Category

Amount (AED)

Fixed Expenses

5,850

Variable Expenses

4,200

Savings & Future

1,950

Total

12,000

Why This Budget Works (Even Though It’s Simple)

- Nothing is extreme

- Lifestyle is still comfortable

- Savings are automatic

- Every dirham has a role

Most importantly, Michael now has control.

He doesn’t need to guess:

- where his money goes

- whether he can afford something

- or why progress feels slow

The budget gives him a clear financial structure without pressure.

This is exactly the point where budgeting becomes practical instead of theoretical.

What Happens Next?

At this stage, Michael knows:

- how much he plans to spend

- how much he plans to save

But one critical question remains:

👉 Does real life actually follow this plan?

That’s where expense tracking becomes essential.

Best Methods for Tracking Expenses

(From Manual Tracking to Digital Tools)

Once a budget is in place, the next challenge is execution. A budget defines intention, but expense tracking reveals reality. Without tracking, even the best budget slowly loses relevance.

Expense tracking does not need to be complex. The most effective method is not the most advanced one — it is the one you can maintain consistently.

Below are the most practical expense tracking methods, commonly used by individuals and professionals in Dubai.

1. Manual Tracking (Notebook or Notes App)

This is the simplest and most underestimated method.

You record every expense manually either in a small notebook or a basic notes app on your phone. Each transaction is written down shortly after it happens.

Best for:

- Beginners

- People who want maximum awareness

- Short-term habit building

Pros:

- Extremely simple

- Builds strong spending awareness

- No tools or setup required

Cons:

- Time-consuming

- Not ideal for long-term analysis

For many people like Michael, starting manually for the first few weeks creates a strong mental connection to spending behavior.

2. Spreadsheet Tracking (Excel or Google Sheets)

This is one of the most widely used methods in financial consulting.

Expenses are recorded daily or weekly into predefined categories. Simple formulas can calculate totals, averages, and deviations from the budget.

Best for:

- Individuals who like structure

- Freelancers and small business owners

- People with variable income

Pros:

- Full control and flexibility

- Easy comparison with budget

- Excellent for monthly reviews

Cons:

- Requires discipline

- Manual input still needed

This method offers a balance between simplicity and analytical power.

3. Budgeting and Expense Tracking Apps

Digital apps automate much of the tracking process. Some connect directly to bank accounts, while others require manual input.

Best for:

- Busy professionals

- People managing multiple accounts

- Long-term tracking

Pros:

- Real-time tracking

- Visual dashboards

- Automatic categorization

Cons:

- Overreliance on automation

- Categories may require adjustment

- Some apps are not fully adapted to UAE banking systems

Apps work best when users review data regularly instead of assuming the app will “handle everything.”

4. Hybrid Method (Most Recommended)

Many financial consultants recommend a hybrid approach:

- Use an app or spreadsheet for structure

- Review expenses manually once a week

This combination keeps awareness high while benefiting from digital efficiency.

Michael adopted this approach. He tracked expenses digitally but reviewed them manually every week. This allowed him to spot patterns early, adjust behavior, and stay aligned with his budget.

What Really Matters in Expense Tracking

The tool itself is not the solution.

Consistency is.

Expense tracking fails when:

- It becomes overly complex

- Reviews are skipped

- Data is collected but never analyzed

Tracking works when:

- Categories are simple

- Reviews are scheduled

- Adjustments are intentional

Expense tracking is not about judgment.

It is about feedback.

The Key Question Expense Tracking Answers

Budgeting asks:

👉 What should happen?

Expense tracking asks:

👉 What actually happened?

When these two answers are compared regularly, financial control becomes practical not theoretical.

Popular Expense Tracking & Budgeting Apps Used in Dubai

In Dubai, expense tracking tools need to work with multiple banks, foreign currencies, and variable income structures. Not every global app performs well in this environment, which is why certain tools are more commonly used than others.

Below are some of the most practical and widely used options among professionals and consultants in Dubai including clients similar to Michael.

1. Sarwa App

(Budget Awareness + Investment Overview)

Sarwa is primarily known as a wealth and investment platform in the UAE, but many users also rely on its app to maintain high-level financial awareness.

While Sarwa is not a pure expense-tracking app, it helps users:

- Monitor account balances

- Understand cash positioning

- Stay conscious of savings and investments

Best for:

People who want budgeting discipline connected to long-term investing, rather than detailed daily expense tracking.

Limitation:

Not designed for granular, transaction-level expense categorization.

2. YNAB (You Need A Budget)

YNAB is popular among expatriates in Dubai who prefer intentional, zero-based budgeting.

Why it works well in Dubai:

- Strong manual control

- Excellent for variable income

- Clear budget-versus-actual comparisons

Pros:

- Forces conscious spending decisions

- Strong educational approach

- Excellent for people rebuilding financial discipline

Cons:

- Requires active engagement

- Bank integrations may be limited in the UAE

YNAB works best for users who are willing to be hands-on.

3. Spendee

Spendee is widely used by Dubai residents who want visual simplicity without complex setup.

Best for:

- Individuals tracking personal expenses

- Couples managing shared costs

- Lifestyle-focused budgeting

Pros:

- Clean interface

- Multi-currency support

- Easy category management

Cons:

- Less analytical depth

- Not ideal for business owners

4. Money Manager

Money Manager is popular among users who want fast, manual entry and offline reliability.

Best for:

- Beginners

- People who want frictionless daily tracking

Pros:

- Extremely simple

- No bank connection required

- High awareness through manual input

Cons:

- Limited reporting

- Not designed for long-term planning

5. Spreadsheet-Based Tracking (Excel / Google Sheets)

Despite the availability of apps, many financial consultants in Dubai still recommend spreadsheets — especially in the early stages.

Why spreadsheets still work:

- Full customization

- Easy currency handling

- Transparent calculations

Michael initially started with a simple spreadsheet before moving to digital tools. This helped him understand his own behavior before relying on automation.

Which Tool Is “Best”?

There is no universal best app.

The best expense tracking tool is the one that:

- Fits your lifestyle

- Matches your income structure

- Encourages regular review

From a financial consulting perspective:

- Apps provide convenience

- Spreadsheets provide clarity

- Habits provide results

A Consultant’s Recommendation

Many professionals in Dubai follow a hybrid approach:

- Use an app for daily tracking

- Review expenses weekly in a simple spreadsheet

- Adjust the budget monthly

This approach combines automation with awareness the exact balance Michael needed to stay in control.

Common Budgeting Mistakes to Avoid

(Mistakes That Quietly Undermine Financial Progress)

Most budgeting failures do not happen because people lack discipline or income. They happen because of small, repeated mistakes that go unnoticed over time. In Dubai’s fast-paced lifestyle, these errors can quietly erode financial progress without triggering immediate alarms.

Below are the most common budgeting mistakes financial consultants see and why avoiding them matters.

1. Making the Budget Too Complicated

One of the fastest ways to fail is building a budget that is too detailed, rigid, or time-consuming. When a budget requires constant adjustments, complex formulas, or daily perfection, it becomes unsustainable.

A good budget should support your life not dominate it.

What works better:

Start simple. Fewer categories. Clear numbers. Improve gradually.

2. Ignoring Variable Expenses

Many people focus heavily on fixed costs like rent and bills, while underestimating variable expenses such as dining, transport, or lifestyle spending. In Dubai, these variable costs often expand quietly.

The problem is not spending it’s spending without intention.

What works better:

Set clear limits for variable categories and review them weekly.

3. Treating Savings as an Afterthought

Saving whatever is “left over” rarely works. In reality, there is almost never anything left over unless savings are planned in advance.

This is one of the biggest reasons people feel financially stuck despite good income.

What works better:

Treat savings like a fixed expense. Automate it if possible.

4. Not Reviewing the Budget Regularly

A budget that is not reviewed becomes outdated quickly. Income changes, expenses shift, and life evolves especially for expatriates in Dubai.

Without reviews, budgets lose relevance.

What works better:

- Weekly expense check

- Monthly budget review

- Quarterly adjustment

Consistency matters more than frequency.

5. Being Too Strict (or Too Flexible)

Extreme discipline leads to burnout. Too much flexibility leads to chaos. Both approaches fail.

A budget should allow room for real life social events, unexpected costs, and personal enjoyment.

What works better:

Build flexibility into the budget intentionally, not accidentally.

6. Relying Only on Apps Without Understanding the Data

Apps are tools not solutions. Many people assume automation replaces awareness. It does not.

If numbers are not reviewed and understood, tracking becomes passive.

What works better:

Use apps to collect data, but review it consciously.

7. Expecting Immediate Results

Budgeting does not create transformation overnight. The benefits compound quietly over time.

Many people quit just before the results begin to appear.

What works better:

Measure progress monthly, not daily. Look for trends, not perfection.

Why These Mistakes Matter

Michael encountered several of these issues early on. What changed his trajectory was not perfection it was correction. Once mistakes were identified and adjusted, his financial progress became steady and predictable.

Budgeting works when it evolves with you.

Budgeting for Short-Term and Long-Term Financial Goals

A budget is not just a tool for controlling expenses. Its real value appears when it connects daily financial decisions to meaningful goals both short-term and long-term.

Many people budget to “stay afloat.”

Very few budget to move forward.

The difference lies in how goals are defined and prioritized.

Short-Term Financial Goals (Stability and Control)

Short-term goals focus on financial stability. They reduce stress, create predictability, and prevent small issues from turning into major problems.

Common short-term goals include:

- Building an emergency fund

- Paying down high-interest debt

- Managing monthly cash flow

- Preparing for planned expenses (travel, relocation, education)

In Dubai, short-term planning is especially important because unexpected costs — rent changes, visa-related expenses, or lifestyle inflation can appear quickly.

A well-structured budget ensures that these goals are funded before discretionary spending takes over.

Key principle:

Short-term goals protect your present financial life

Long-Term Financial Goals (Growth and Security)

Long-term goals are about financial growth and future independence. They require patience, consistency, and a budget that supports long-term thinking.

Typical long-term goals include:

- Retirement planning

- Investment accumulation

- Business expansion

- Wealth preservation

- Financial independence

These goals cannot be achieved through occasional effort. They depend on regular contributions that are built directly into the budget.

Michael realized that without long-term planning, his income would support his lifestyle but not his future. Once he treated long-term goals as non-negotiable budget items, progress became measurable.

Key principle:

Long-term goals are built quietly, month by month.

How Budgeting Connects Both Time Horizons

The most effective budgets do not choose between short-term and long-term goals they balance both.

A healthy budget typically:

- Covers fixed and variable living expenses

- Funds short-term stability goals

- Allocates resources to long-term growth

When one area is ignored, imbalance appears:

- Too much focus on today → no future progress

- Too much focus on the future → burnout and frustration

Budgeting provides a framework where both timelines coexist.

A Practical Goal-Based Budgeting Mindset

Rather than thinking in categories alone, many financial consultants encourage thinking in purpose-based allocations:

- Money for living

- Money for protection

- Money for growth

This mindset helps avoid emotional spending decisions and reinforces intentional behavior.

Michael adopted this approach and noticed a shift: spending became easier to justify, saving felt purposeful, and financial decisions became calmer.

Why This Matters in Dubai

In a city driven by opportunity and speed, it is easy to prioritize lifestyle over long-term security. Budgeting forces a pause a moment to decide what truly matters.

A budget aligned with goals does not limit freedom.

It creates direction.

Tools and Apps for Budgeting and Expense Tracking

(Choosing Tools That Support Not Replace Your System)

Budgeting and expense tracking do not succeed because of tools alone. They succeed when tools support a clear system and consistent habits.

Many people spend more time searching for the “perfect app” than actually managing their money. In reality, the best tool is the one that fits your lifestyle, your income structure, and your willingness to review data regularly.

In Dubai, where people often manage:

- multiple bank accounts

- foreign currencies

- variable income sources

tools must remain simple, flexible, and reliable.

What to Look for in a Budgeting or Tracking Tool

Regardless of whether you use an app, spreadsheet, or hybrid method, an effective tool should:

- allow clear expense categorization

- support manual adjustments

- make monthly reviews easy

- avoid unnecessary complexity

Tools should reduce friction, not add to it.

Apps vs Spreadsheets: Which Is Better?

From a financial consulting perspective:

- Apps are excellent for daily convenience

- Spreadsheets are powerful for monthly clarity

That is why many professionals recommend a hybrid approach:

- Track daily expenses using an app

- Review and analyze data monthly using a simple spreadsheet

This approach keeps awareness high while maintaining analytical control.

The Most Important Rule

No tool can fix poor habits.

No automation can replace understanding.

The purpose of tools is not to think for you it is to give you clear feedback so you can make better decisions.

When tools are used intentionally, they become enablers.

When used passively, they become distractions.

Conclusion: Budgeting Is Where Financial Control Begins

Michael did not change his financial life by earning more money.

He changed it by learning how to direct what he already earned.

His story reflects a common reality in Dubai. Many people arrive with strong income potential and real opportunities, yet struggle to make meaningful financial progress. The issue is rarely income. It is structure.

Budgeting and expense tracking are not about restriction or control for the sake of control. They are about clarity. They help transform money from a source of stress into a tool for stability, growth, and long-term security.

Once Michael understood where his money was going and why his financial decisions became calmer, more intentional, and more effective. Small daily choices stopped working against him and started working for him.

This is the real power of budgeting:

- It connects daily spending to long-term goals

- It prevents silent financial erosion

- It creates direction in an environment full of distractions

Whether you are an individual professional, a business owner, or newly settled in Dubai, budgeting is not optional if you want sustainable progress.

At Daraltharwa, financial consulting always begins with this foundation not because it is basic, but because it works.

A Final Thought

You do not need a perfect system to start.

You need a simple one you can maintain.

If Michael’s journey feels familiar, budgeting may be the first step toward turning income into lasting financial clarity.