Financial Advice in Dubai Is Not What You Think

Dubai is a major financial opportunity for migrants, but at the same time, it is one of the most complex financial advisory markets in the world.

A Migrant’s Guide to Choosing the Right Advisory Model

Dubai is a major financial opportunity for migrants, but at the same time, it is one of the most complex financial advisory markets in the world.

For most expats, the real problem is not:

- how much they earn, or

- what they invest in.

The real problem is this:

they don’t know which advisory model they have entered when they make financial and investment decisions.

In Dubai, a large share of what is offered under the label “Financial Advisory”

is, in practice, Brokerage or Sales Advisory—not true advice.

The Opportunity Is Real, But Mistakes Are Expensive

For many migrants, Dubai is the first place where they:

- earn in USD or multiple currencies,

- do not pay direct personal income tax,

- gain access to international financial products and global investment opportunities.

But these advantages, when combined with the wrong type of financial advice,

can lead to decisions that look profitable on paper—

and turn costly in the long run.

The key point is this:

in recent years, regulators, financial professionals, and even international media have repeatedly pointed out that

a significant share of expat financial losses comes not from markets, but from the wrong advisory model.

Not because people were low-income,

but because they didn’t realize what kind of financial relationship they were entering.

Why This Article Matters

This article is not here to tell you:

- which product is better, or

- which market will deliver the highest returns.

The goal is to clarify:

which financial advisory methods actually work for migrants in Dubai,

and which models—even if common—can become high-risk and expensive.

From here onward, we separate the “product” from the “method”and focus on the logic, incentives, and structure of financial and investment advice.

Real Financial Advisory vs Brokerage or Sales Advisory in Dubai

In Dubai’s financial market, the term “Financial Advisory” is used widely,but in practice it can refer to two very different models with dramatically different outcomes for migrants.

Understanding this difference is one of the most important ways to avoid costly long-term decisions.

1: Decision Philosophy: Where Does the Solution Start?

Brokerage / Sales Advisory

In this model, the decision path is usually predetermined.

The investment product or structure is often defined upfront, and the process is designed so the client eventually ends up there.

Financial analysis plays an instrumental role, not a decisive one.

The main objective is executing the transaction.

In contrast,

Real Financial Advisory

starts with the person’s financial reality—not with a ready-made solution.

It examines:

- income structure,

- time horizon,

- residency and tax situation,

- true risk tolerance (not the claimed one).

The final solution may include investing or it may not.

2: How the Advisor Gets Paid (Incentives and Conflict of Interest)

In brokerage models, the advisor’s income is directly tied to transactions. This means:

- there is a built-in incentive to sell,

- no transaction often means no revenue,

- even with good intentions, the structure creates a conflict of interest.

In real financial advisory,the advisor is paid via a transparent, pre-agreed fee.

This fee is independent of buying or selling products, which allows the advisor to recommend not acting when that is the best decision.

3: Time Horizon and Continuity of the Decision

Brokerage often treats decisions as one-time events:

a purchase, a contract, a capital transfer.

After that, the relationship is often limited or ends.

Real advisory treats decisions as part of a longer path.

A decision made today must:

- remain reviewable in the future,

- adapt to life changes,

- withstand changes in country or regulations.

That is why monitoring and re-adjustment are integral to this model.

4: Tax and Legal Structure (Critical for Migrants)

One of the most decisive differences is how each model treats tax.

In many brokerage models:

- tax is treated as the client’s personal responsibility,

- there is no deep review of tax residency or reporting,

- decisions are built for “today’s situation.”

In real advisory:

- tax is part of the decision design,

- residency and exit scenarios are examined,

- long-term tax consequences are made explicit.

For migrants, this alone can determine success or failure.

5: What Is the Output of the Advice?

In brokerage, the output is typically clear:

- a product,

- a contract,

- an investment completed.

In real advisory, the main output is different:

- a decision framework,

- the logic behind choices,

- review criteria, and then if needed the right instruments.

The focus shifts from “what to buy” to “why and how to decide.”

6: Accountability for Outcomes

In brokerage, responsibility is often limited to correct execution.

Long-term performance is outside the scope of commitment.

Real advisory defines accountability at a higher level:

- defending the logic of the decision,

- full clarity on risks,

- ongoing support for review and correction.

This is the line between selling and advising.

Summary

Brokerage is legal and common,

but it is not financial advice in the true sense.

For Dubai migrants whose financial lives are tied to more than one country,

choosing the wrong advisory model can create costs that only become visible years later, in another jurisdiction.

In the rest of this article, we will examine which advisory methods are actually more effective for migrants in Dubai, and why.

Method 1 — why Fee-Based advice changed every thing

Why This Is the Right Starting Point

For many migrants in Dubai, the first encounter with “financial advice” often begins with an investment pitch.

This is not accidental—it is the result of a model where the advisor’s income is tied to product sales.

Fee-Based Financial Advisory intentionally reverses this logic.

In this model, the advisor is not paid for what you buy,

but for analysis, thinking, and designing your financial path.

That small difference changes the entire relationship.

How This Method Works in Practice

In a fee-based model:

- the advisory fee is clear and agreed upfront,

- the advisor’s income is not tied to any product transaction,

- recommending “do nothing for now” is fully valid.

The process typically starts with questions like:

- What are the most important financial decisions in your life?

- Which risks are acceptable, and which are irreversible?

- How do your income, liquidity, mobility, and tax situation interact?

Until these answers are clear,

moving to a product or investment decision is premature.

Why This Matters Specifically for Dubai Migrants

A migrant’s financial life is rarely tied to one country. Many face:

- temporary or changing residency,

- multi-currency income,

- assets spread across countries,

- a realistic chance of relocation or exit.

In these conditions, product-driven decisions are fragile.

An investment may perform well,

but the structure around it can collapse when country or regulations change.

Fee-based advisory shifts focus from “short-term returns” to:

- decision logic,

- structural durability,

- long-term adaptability.

That is why in mature advisory markets

like Europe, Canada, and Australia, this model is often considered the standard.

Practical Signs You’re in a Real Fee-Based Relationship

In a real fee-based relationship:

- the first session is about understanding you—not presenting products,

- the outcome may be “do nothing yet,”

- the advisor can clearly explain why an option is not suitable.

If these do not happen,

you are likely in a sales-driven model—even if it is called “advisory.”

Why This Is Only the Starting Layer

Fee-based advisory alone is not the answer to everything.

But it is the foundation for more advanced methods, such as:

- tax-aware advisory,

- goals-based planning,

- discretionary management,

- hybrid and intelligent models.

In the next section, we move to a method that can be even more critical for migrants: Tax-Aware Financial Advisory.

Method 2 - Why Tax-Blind Advice Fails Migrants?

A Simple but Precise Definition

Tax-aware financial advisory means every financial decision—before it touches “products” or “returns”—passes through one fundamental question:

What are the tax consequences of this decision across different residency scenarios and my next country?

In this method, tax is not a “final note.”

It is one of the pillars of the decision design.

Why This Method Is Vital for Dubai Migrants

Many people in Dubai assume:

“Because the UAE has no personal income tax, tax is not a major factor.”

But migrants typically live a multi-jurisdiction financial life.

Assets, income, investments, and future relocation can tie them to several countries.

This is exactly where tax-blind decisions generate costs years later.

What This Method Actually Examines

Before any investment recommendation, tax-aware advisory clarifies:

Tax Residency

- Where are you currently a tax resident?

- Is this stable, or likely to change?

Cross-Border Exposure

- What is your citizenship?

- Where does your income come from?

- In which countries are your assets held?

Withholding Taxes

Even if Dubai does not tax you, many countries apply withholding tax on:

- dividends,

- bond income,

- certain investment earnings.

Reporting & Compliance

In some countries, simply holding foreign accounts or assets can create reporting obligations—even if you made no profit.

Exit / Relocation Scenarios

- What happens if you move to Europe/Canada/Australia in 3 years?

- What if you return to your home country?

- Could today’s growth become tomorrow’s heavy tax burden?

The Difference Between Real Tax-Aware Advice and “A Tax Mention”

Real tax-aware advice means:

- tax is embedded in the decision design,

- future scenarios are actively examined,

- the tools and holding structures are chosen to survive a country change.

In shallow models, the advisor ends with:

“Tax matters too—check it yourself.”

That is not tax-aware advice. That is shifting responsibility.

What This Method Achieves for Migrants

This method helps:

- reveal hidden costs,

- keep decisions defensible and sustainable,

- build an international structure—not just a product selection.

And one key point:

Tax-aware advisory is usually strongest when built on fee-based advice, because sometimes the best tax decision is:

- don’t buy yet,

- restructure first,

- or choose a different instrument.

That is hard to say inside a sales-driven model.

Two Stories to Make It Concrete

Michael Is Leaving (From Dubai to Canada)

Michael is 41, English-speaking, spent 5 years working in Dubai, and built strong income. In Dubai:

- no personal income tax,

- his investments grew,

- he assumes “everything is fine.”

story 1:Michael works with an “advisor” who is largely sales-led. Sessions quickly focus on:

- international investment products,

- pre-built portfolios,

- return-focused narratives.

No one seriously asks:

“What happens if you leave Dubai in 3 years?”

Three years later, Michael moves to Canada and becomes a Canadian tax resident. Suddenly, he learns:

- Canada cares about worldwide income,

- capital gains and investment income can become taxable,

- some of his previous structures are not tax-efficient.

Michael says:

“I didn’t pay tax in Dubai.why am I paying so much now?”

The answer:

because decisions were designed for “Dubai today,” not for “Michael’s multi-country life.”

If tax-aware advisory had been in place from the beginning:

- relocation scenarios would have been part of the plan,

- holding structures and instruments would have been chosen with the future in mind,

- the tax shock and complexity would have been dramatically reduced.

Story 2: Michael Is Staying (Long-Term in Dubai)

Now assume Michael decides:

“I’m staying in Dubai for at least 10–15 years.”

He thinks:

“Then tax-aware advice isn’t needed—there is no tax here.”

But as his wealth grows, real issues appear:

Hidden challenges for long-term residents:

- some investments carry withholding tax,

- holding everything personally creates legal and planning risks,

- inheritance, asset protection, and transfer planning becomes relevant,

- any residency change or regulatory shift can expose fragile structures.

If Michael had tax-aware advisory:

- instruments with lower indirect tax friction could be selected,

- ownership and holding structure would be designed more professionally,

- decisions would stay durable، not just “good for now.”

Very Short Summary

Tax-aware advice is not only for people leaving Dubai.

For leavers: it prevents future tax shocks.

For stayers: it builds durable structures and controls indirect taxes.

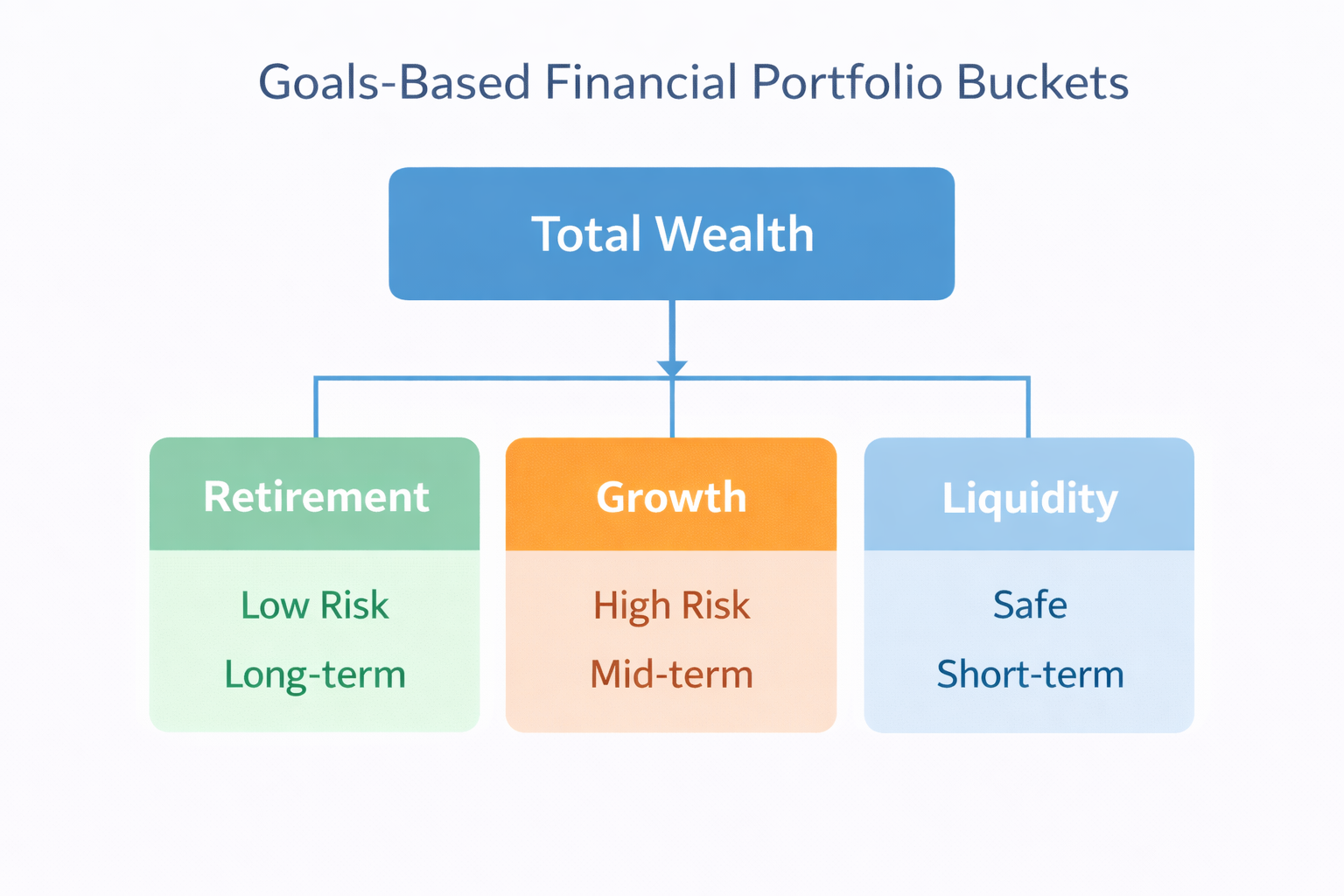

Method 3 — Plannig Around Life , Not Just Return

Where This Method Starts

Unlike many common models, goals-based planning does not begin with:

“What should we invest in?”

It begins with:

“What do you want this money to do for your life?”

In this method, returns are not the real goal.

The goal is achieving real-life outcomes with minimal irreversible risk.

The Fundamental Difference from Traditional Models

In traditional models:

- risk tolerance is a number,

- the portfolio becomes the center,

- everything revolves around performance.

In goals-based planning:

- risk = the probability of failing a goal,

- each goal has its own horizon and risk level,

- money is a tool—not the destination.

So a person may be:

- conservative for retirement,

- risk-seeking for growth,

- fully safe for liquidity,

all inside one integrated plan.

Why This Works Especially Well for Dubai Migrants

For many Dubai migrants, financial life is not linear or fully predictable.

Unlike someone who lives their whole life in one country, migrants face linked, changing decisions.

For them, the future is not a single scenario.

The Reality of Migrant Financial Life

Migrant financial life is often:

not linear

It may include staying, relocating, returning, or migrating again.

Today’s decisions may show their full impact in another country.

not fully predictable

Job changes, residency rules, family circumstances, or migration policies can change the path.

full of multi-step decisions

A single financial decision depends on what comes next:

- What if I stay?

- What if I leave?

- What if I start a business?

In these conditions, plans built purely around “investment returns” lose relevance quickly.

The Core Advantage of Goals-Based Planning

This method is built for uncertainty. It ensures:

- decisions are linked to specific life goals,

- each goal has its own horizon and risk,

- success is measured by goal achievement probability—not only return.

Instead of one portfolio, you build parallel tracks each with a defined purpose.

Key Benefits for Dubai Migrants

- Flexibility under relocation or life changes

If goals are defined, relocation does not collapse the plan only parts get adjusted. - Less emotional decision-making

When each bucket has a purpose, market volatility triggers less panic. - Clear prioritization

Migrants often have multiple goals. This method clarifies what is non-negotiable vs flexible. - Risk separation instead of risk concentration

Risk is distributed across goals rather than forced into one strategy. - Defensible decisions

When decisions are goal-linked, they remain rational even in bad market years.

Michael’s Story - What This Adds Beyond the Previous Methods

Before goals-based planning, Michael had already used:

- Fee-based advisory (to escape sales pressure),

- Tax-aware advisory (to reduce future tax risk).

But he still had a gap:

“I know what not to buy—

but I don’t clearly know where my money needs to take me.”

With goals-based planning, the focus moves from structure and risk to meaning. Early sessions include:

- no talk about ETFs or markets,

- focus on Michael’s life, not his portfolio.

Goals become clear:

- family financial security (non-negotiable),

- career flexibility within 5 years,

- ability to relocate again without financial pressure,

- growth—but only within those boundaries.

The difference for Michael:

Before: logical but fragmented decisions

After: decisions connected to goals

Before: relative calm

After: durable calm

Before: risk management

After: life-level financial management

Michael finally feels:

“My money has a path, not just returns.”

Summary of This Method

Goals-based planning works well for Dubai migrants because:

- it adapts to uncertainty,

- it keeps decisions human and life-centered,

- it gives money meaning—not just numbers.

Method 4 - When Good Decisions Still Fail

Who This Method Is Built For

Not everyone wants or can:

- make decisions every month,

- follow markets constantly,

- analyze every change in residency or regulation.

Many Dubai migrants are:

- entrepreneurs,

- executives,

- or people whose income depends on mental focus.

For them, the biggest risk is not ignorance—it’s lack of time and consistent follow-through.

Discretionary asset management is designed for that reality.

A Simple but Accurate Definition

In this method, the investor:

- designs the decision framework with the advisor/asset manager (risk, goals, constraints, horizon),

but daily execution is delegated to the manager.

Meaning:

- big decisions remain yours,

- execution decisions are handled by the manager,

- everything stays within a pre-agreed framework.

No emotional trading. No impulsive decisions.

How This Differs from “Handing Your Money to Someone”

Many people misunderstand discretionary management as:

“I gave someone my money and they can do whatever they want.”

That is the most dangerous misconception.

In a professional discretionary model:

- the manager cannot act outside the framework,

- the framework is legally defined and explicit,

- reporting, transparency, and the ability to stop exist,

- ownership always remains yours.

If these are missing, this is not discretionary management—it’s risk.

Why This Matters for Dubai Migrants

Migrant life is full of interruptions and shifts:

- flights,

- relocation,

meetings,

- travel,

- work pressure,

- country changes.

In this reality, even the best plan fails without execution.

Discretionary management helps ensure:

- decisions execute even when you are unavailable,

- risks are adjusted on time,

- opportunities are not missed,

- the framework survives, even when you are not present.

The Difference from Standard Advisory

In standard advisory:

- the advisor suggests,

- you execute,

- timing and discipline are on you.

In discretionary management:

- the framework is built with you,

- execution is handled by the manager,

- follow-through responsibility is removed from your shoulders.

For many migrants, this difference is decisive.

The Big Danger - Delegation Without a Proper Foundation

This method only works properly when it is built on:

- fee-based advisory,

- tax-aware design,

- goals-based planning.

Without these:

delegation of execution becomes delegation of risk—

and that is where disasters happen.

Signs of Healthy Discretionary Management

If you see these, the setup is likely sound:

- the framework is written,

- risk level is measurable,

- reports are regular and understandable,

- stopping or changing is possible,

- the manager can explain why actions were taken.

If these are missing:

you don’t have asset management—you have hope.

What This Delivers for Dubai Migrants

For many migrants, discretionary management creates:

- mental clarity,

- consistent execution,

- lower behavioral risk,

- the ability to focus on life and work.

But only if it is delivered:

within the right framework,

with transparency,

and without conflicts of interest.

Michael’s Story - When the Decision Is Right but Execution Fails

After Michael had:

- fee-based advisory,

- tax-aware advisory,

- goals-based planning,

everything was structurally correct.

The problem was simple: Michael had no time.

He was a senior executive—constant travel, back-to-back meetings, time zone changes, urgent business decisions.

His plan was correct, but execution was:

- late,

- inconsistent,

- sometimes not done at all.

He knew:

- what to buy,

- what not to buy,

- when to reduce risk.

But knowing was not enough.

Breaking point:

In a market volatility period, a decision that needed execution within 24 hours

was delayed by 3 weeks—

not because of analysis, but because of life.

Result:

risk increased, opportunity was missed, and a carefully designed structure was damaged.

That’s when Michael realized:

the issue wasn’t decision-making anymore—

it was ownership of execution.

With discretionary management, Michael delegated execution—not decision-making.

The manager:

- acted within the framework,

- adjusted risk on time,

- traded without emotion,

- provided transparent reporting.

Michael only needed to:

- supervise,

- participate in big decisions,

not daily details.

Before:

right decisions, inconsistent execution, constant stress, missed opportunities.

After:

right decisions, consistent execution, controlled risk, mental calm, stable goal progress.

Michael finally feels:

“my financial system works—even when I’m not there.”

Method 5 -Where Human Advice Needs Machine Support

Why This Method Exists

The previous methods are strong, but they share one limitation:

they depend on human cognitive capacity.

In the real world of Dubai migrants:

- assets span countries,

- income spans currencies,

- regulations keep changing,

- markets move 24/7,

- decisions are interconnected.

No human—even the best advisor—can:

- see all scenarios at once,

- compute all consequences in real time,

- update decisions perfectly and consistently without fatigue.

This is where hybrid models emerge.

A Simple and Precise Definition

Hybrid advisory means:

human judgment + machine computation

In this model:

- humans define goals, meaning, and risk boundaries,

- machines handle data, scenarios, monitoring, and optimization.

AI does not replace the advisor.

AI does not replace the decision.

AI does not replace the human.

AI handles what humans are weak at:

- multi-scenario computation,

- continuous risk monitoring,

- early warnings,

- fatigue-free optimization,

- reducing repetitive behavioral mistakes.

What This Method Improves

In hybrid models, decisions are not only “right”—they are also timely.

Risks are detected before they become crises.

Opportunities are spotted before they disappear.

Decisions adapt as life changes.

This is especially important for migrants because their lives contain constant unpredictability.

Hybrid vs Robo-Advisor

Robo sees numbers.

Hybrid understands meaning too.

In robo models:

- everything is delegated to an algorithm,

- goals are simplified,

- complex life realities are ignored.

In hybrid models:

- goals remain human,

- ethical and logical constraints stay intact,

- AI is a tool—not the decision-maker.

The Big Danger — AI Without Human Advisory

If AI is used without a human framework:

- the system may optimize but become ruthless,

- it may miss irreversible risks,

- it may make decisions that are numerically correct but humanly wrong.

That’s why real hybrid models sit on:

- fee-based foundations,

- tax-aware design,

- goals-based planning,

- healthy discretionary execution.

Why This Is the Future Standard

Because expat financial complexity is no longer manageable with purely traditional tools.

Not due to lack of information—

but due to too much information.

Hybrid models distribute the load:

humans provide meaning, machines provide discipline, and the system remains stable.

Michael’s Story — When Decisions Outrun Human Capacity

Michael now had:

- a framework,

- a plan,

- delegated execution.

But a new problem emerged:

the number of decisions exceeded his mental capacity.

Assets in multiple countries, income in multiple currencies, legal changes, and multiple goals moving at once—

even the best asset manager couldn’t evaluate every consequence instantly.

With hybrid advisory:

AI monitored Michael’s scenarios daily,

flagged hidden risks earlier,

simulated the impact of regulatory or FX changes,

and proposed optimization ideas.

But the final decision remained human:

Michael and his advisor—within a clear framework.

Result:

faster decisions, fewer behavioral errors, and more mental calm.

Michael says:

“For the first time, I feel my financial system is ahead of me—not behind.”

A Practical Checklist for Dubai Migrants

How to Know What Model You’re Actually In

Before any financial or investment decision, ask yourself:

“Am I receiving real advice—or am I being guided toward a sale?”

With this checklist, you can tell in 10 minutes.

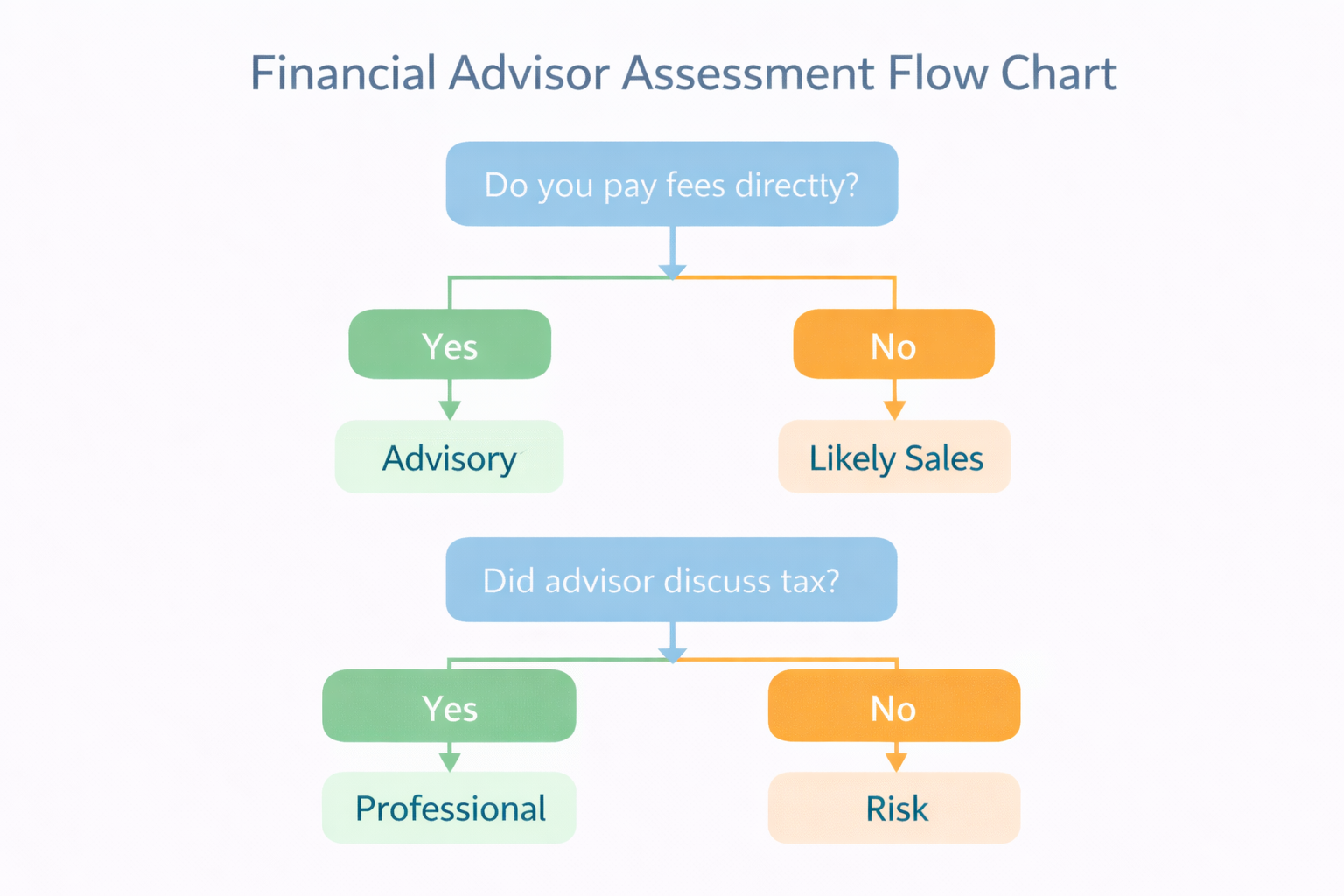

1) Where Does the Advisor’s Money Come From?

If:

- advisor income depends on product purchase → Sales / Brokerage

- a clear fee is agreed upfront and independent → Fee-Based Advisory

⚠️ If the answer is not transparent, a conflict of interest likely exists.

2) What Was the First Meeting About?

If:

- the first meeting moved to products, portfolio, returns → sales-driven

- the first meeting focused on life, income, risk, plan → real advisory

Real advisory starts with questions—not pitches.

3) Is “Doing Nothing” a Valid Option?

If:

- you must always do something → sales-driven

- sometimes the advice is “wait” → real advisory

An advisor who cannot say “no” is not advising.

4) Where Does Tax Sit in the Decision?

If:

- tax is mentioned at the end → superficial

- tax is embedded in design → tax-aware advisory

For migrants, this is critical.

5) Did Anyone Ask About Your Next Country?

If:

- nobody asked what happens if you leave Dubai → hidden risk

- relocation scenarios were examined → professional advisory

Advice that can’t see the future won’t get today right either.

6) Were Your Goals Defined?

If:

- you only have a portfolio → product-driven

- you have goals, timelines, priorities → goals-based planning

Returns without goals are just numbers.

7) Who Executes?

If:

- everything depends on you → basic advisory

- execution is delegated within a framework → discretionary management

If you have no time, this difference matters.

8) How Does Monitoring and Reporting Work?

If:

- reporting exists only when you ask → weak

- regular, understandable, proactive reporting exists → professional

No reporting = no control.

9) How Is Technology Used?

If:

- it’s only spreadsheets and WhatsApp → traditional

- risk monitoring, warnings, and scenario analysis exist → hybrid / AI-assisted

Modern complexity requires modern tools.

10) What Happens If You Stop Working Together?

If:

- everything collapses → dangerous dependency

- the framework remains → real advisory

Good advice doesn’t make you dependent—it makes you stronger.

Quick Summary

The more “yes” answers you have on the right side,

the healthier, more sustainable, and more professional your advisory model is.

If you hear more “no” answers,

the problem isn’t you—it’s the model.